Market Intelligence

March 16, 2026

.png)

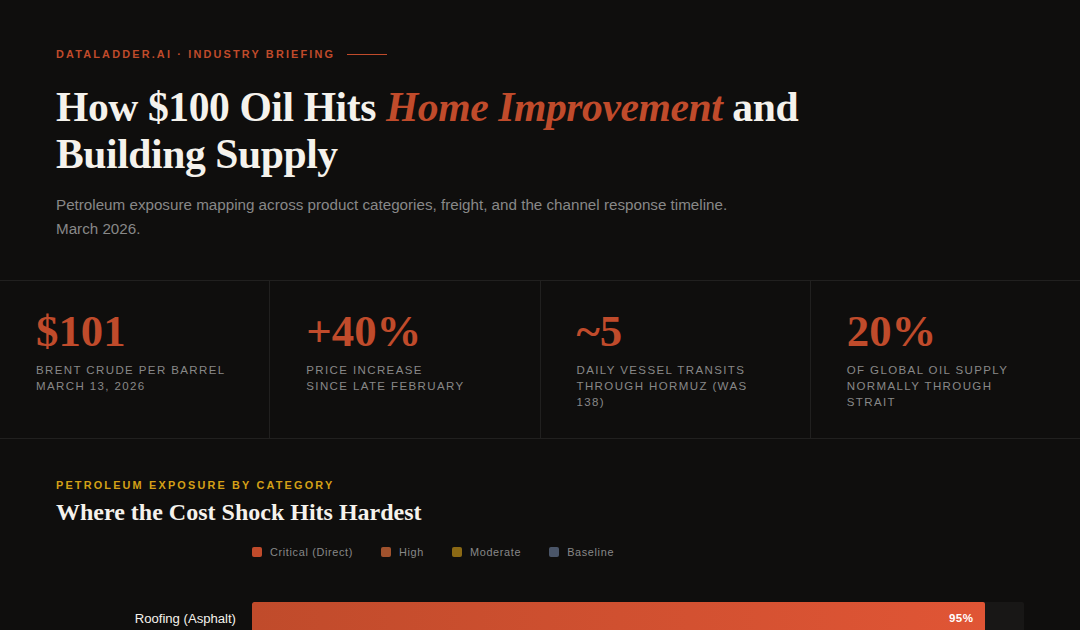

Brent crude hit $101/barrel on March 13, 2026, up nearly 40% since late February. The trigger: US-Israeli strikes on Iran and Iran's closure of the Strait of Hormuz, through which roughly 20% of global oil supply normally flows. Traffic through the strait has fallen from 138 daily vessel transits to fewer than five. This is the largest disruption to global energy supply in a generation, and it is not resolved.

Oil at $100 a barrel is not an abstraction for home improvement and building supply manufacturers. It is a direct cost shock running through almost every input in your supply chain: resins, adhesives, coatings, foam, vinyl, asphalt, lubricants, freight, and more. And it arrives at a moment when the industry was already navigating softening housing demand and margin pressure from two years of inventory normalization.

The manufacturers that will come out of this period in the best position are the ones who move fast on visibility: who sees the price moves first, which categories are most exposed, where competitors are absorbing versus passing through, and how the channel is responding. Speed of insight is speed of action.

The home improvement and building supply category is unusually petroleum-dependent. Unlike appliances or furniture, many of the core product categories are either petroleum-derived or require significant hydrocarbon-based inputs in manufacturing or transport. The cost shock does not hit evenly.

Roofing is the most direct hit. Asphalt shingles are petroleum-based, and asphalt costs typically track oil prices with a 30 to 60 day lag. Manufacturers like GAF, Owens Corning, and TAMKO will feel this in COGS almost immediately. Vinyl siding, PVC pipe and fittings, plastic decking, foam insulation, caulks and sealants, and paint are all petroleum-derived or heavily petrochemical-dependent.

Doors and windows carry dual exposure: vinyl frames and foam insulation cores are petroleum-based, and the energy cost of glass production is significant. Plumbing is heavily PVC and CPVC. Adhesives, grouts, coatings, and waterproofing membranes across every category contain petroleum-derived ingredients.

Diesel tracks crude oil directly. Every pallet moving through ABC Supply, Home Depot's distribution network, or a regional two-step distributor costs more. Freight typically runs 3 to 7% of cost of goods in this industry. A 30 to 40% increase in diesel turns a 5% freight line into a 6.5 to 7% freight line overnight. For manufacturers running on 8 to 12% gross margins at wholesale, that is material.

Oil-to-input cost transmission is not instantaneous. Asphalt and resin pricing typically lags crude by 30 to 60 days due to contract structures and inventory buffers. This means manufacturers have a narrow window right now to reprice, renegotiate, or hedge before the full cost wave hits their P&L.

When input costs spike, the entire channel reacts, and not always in the way manufacturers expect or want. Understanding the sequence of channel behavior is critical to positioning correctly.

Home Depot and Lowe's will not absorb cost increases quietly. Their buyers know the oil price move is real, but they will negotiate the percentage pass-through hard, demand phased timelines, and use the opportunity to push private label alternatives. The manufacturer that arrives at that negotiation with clean data (actual cost build-up tied to oil price, competitor pricing intelligence, category margin context) negotiates from strength. The one that shows up with a letter asking for 8% will get cut to 4%.

Wholesale distributors, including ABC Supply and regional two-steppers, will reduce forward buying on high-cost-exposure SKUs. They have been burned on inventory in volatile cost environments before. This means manufacturers may see a demand air pocket in weeks 4 through 10 as distributors draw down existing stock before reordering at new prices. Do not mistake this for a demand problem. It is a behavioral pattern.

Any time branded manufacturers raise prices, the price gap between branded and private label widens. Oil at $100 gives Menards, Home Depot, and regional chains a clear narrative to push their own brands. Monitoring private label pricing and shelf presence across your categories right now is not optional. It is competitive intelligence that directly affects your category review outcomes.

The manufacturer who arrives at the retailer price negotiation with data wins. The one who arrives with a letter asking for 8% gets 4%.

Every cost shock creates information asymmetry. Some manufacturers see the full picture: their own exposure, competitor moves, channel behavior, private label positioning. Most see a fraction of it and make decisions in the dark.

The specific intelligence that matters right now includes SKU-level price tracking across retail and wholesale, private label shelf presence monitoring, distributor inventory data, competitor promotional activity (are they discounting to hold volume?), and ratings and review patterns (do consumers start downgrading products they perceive as poor value at higher price points?).

This is exactly the kind of multi-channel, real-time intelligence that syndicated providers like Circana and Datavations cannot provide. They have no wholesale coverage, no distributor data, and no real-time pricing layer. The oil shock makes the wholesale and pro channel blind spot more dangerous than ever, because that is where the demand signal and the price signal are going to move first.

Pro and wholesale channels will see the demand impact of $100 oil before retail does. Contractors defer projects, distributors tighten orders, pricing shifts faster without retail buyer gatekeeping. If your data infrastructure does not cover wholesale, you are flying blind during the most volatile cost environment in years.

The Strait of Hormuz situation is unpredictable by definition. It depends on military and diplomatic developments that no analyst can forecast with confidence. J.P. Morgan's long-run Brent forecast remains around $60/barrel based on structural supply surplus, which suggests that once the geopolitical shock resolves, prices could retrace significantly. But "once it resolves" is doing a lot of work in that sentence.

What that means practically: prepare for a 60 to 120 day elevated oil environment at minimum. Protect margin on the way up. Do not make long-term pricing commitments at current input cost assumptions. Watch the Strait daily. When vessel transits start recovering toward normal, that is your signal that the price peak may be close.

But do not let the unpredictability of the macro situation become an excuse for inaction on the commercial side. The retailers and distributors you deal with are making decisions right now. If you are not at that table with data, someone else is.

Talk to our team about how SKU-level visibility can help your business.

Copyright © Insight 2026